The science behind property market forecasting

Promoted by Propertyology.

The frequent inaccuracy of property market forecasts by banks and economists (the world’s biggest generalisers) is cause for taking much of what they say with a grain of salt.

In about October every year, national market analysts forecast where they think each major capital city is headed in the calendar year ahead.

Those predictions are based on an understanding of a number of variables however, most analysts tend to rely too heavily on current market activity if you ask me.

Don’t get me wrong, forecasting is difficult. Can you think of anything more difficult than trying to predict human behaviour?

Plus, those of us who are prepared to publish our forecasts risk facing public ridicule when it’s proven that the crystal ball didn’t work.

The reality is that no one is always right!

But, before even reaching the half way point of this year, several analysts had already slashed their initial predictions for several capital cities. The thing is, there’s been no material change to market fundamentals since late last year. The only reason for adjusting their forecasts is that, yet again, their initial assessment was out of whack.

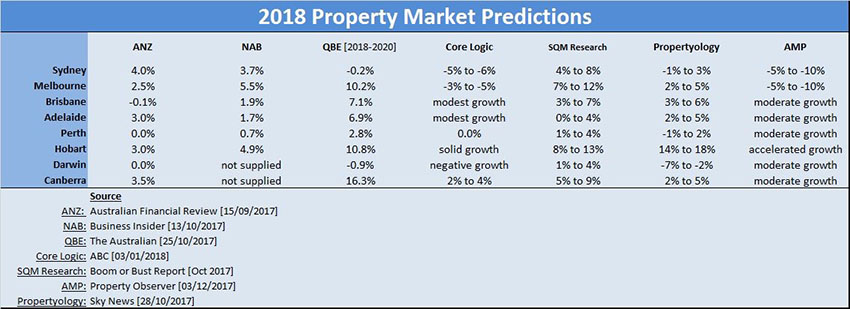

This chart is a summary of what several of Australia’s biggest profile anlaysts, including Propertyology, forecast for capital cities in 2018.

While several analysts appeared to believe that the price decline that commenced in Sydney in August 2017 would bounce back and that Melbourne would remain strong, we considered that to be wishful thinking more than anything.

When Propertyology published its 2018 capital city forecasts in October 2017, we felt that zero growth was probable for Sydney and Perth, that Darwin’s three-year decline would accelerate lower, Hobart would have another stellar year with growth in the mid-to-high teens, and the other capital cities would be bunched together on two to five per cent growth for the year.

As I mentioned, current activity is a factor in forecasting, but the art is to look beyond what is actually occurring within a market and focus more on the numerous factors that influence change within a market. Propertyology’s aim is to anticipate what might happen next. We are trying to join the dots of a dozen or so moving parts.

Nationally,these include potential interest rate fluctuations, credit policy, what the Australian dollar might do,the tone of the mainstream media, and implications of any new tax policies.

Then there are international considerations: what will China, Trump, or North Korea do? Plus, there’s economic knock-on effects from things like trade agreements and commodity prices to consider, too.

If that wasn’t enough, state and individual city factors are then taken in to account. Things like election promises, property initiatives such as grants and stamp duty changes, housing supply (current and in the pipeline), migration trends, local sentiment, industry trends, job trajectories, and major projects.

Easy-peasy? I wish!

In attempting to join all of these moving parts together we are painting a “picture”(positive, negative or unchanged) of a chosen market in the foreseeable future.

It’s a science, but it’s by no means an exact science.

Resisting the temptation to focus solely on current market performance and more on factors likely to influence change enabled Propertyology to forecast a [2013] recovery in capital city property markets following two years of price declines.

It’s why [in 2014] we disagreed with the masses who claimed Brisbane was set to follow in Sydney’s footsteps and boom. And, it’s also how we correctly forecast Perth’s prolonged trough before its downturn occurred [2015].

This current underwhelming performance of seven out of eight capital city markets was anticipated by Propertyology a few years ago [2015].

That’s not to say we are perfect though. For example, in 2016 we released a research report urging investors to be cautious about Melbourne’s property market.

We expressed concern that the loss oftens of thousands of car manufacturing jobs and an all-time record housing supply pipeline might have. Our report stated that ‘…2017 and 2018 look particularly bleak…’ for Melbourne. What we didn’t count on at the time was a huge influx of interstate migrants from Western Australian to Melbourne. Maybe we were overly cautious. Or maybe history will just prove that our forecast was just 12 months ahead of its time (Melbourne’s downturn officially commenced in December 2017).

Propertyology’sthirst for joining dots, as opposed to merely adopting the consensus view, is done out of sincere passion for helping everyday Aussies to make informed property investment decisions.

Arguably our proudest legacy of our daily commitment to this process was our ability to forecast Hobart’s property market upswing when [in 2014] absolutely no one else did.

During a post-GFC era when there’s been very few locations throughout Australia where property markets have been strong, the university city of Hobart and newly-found tourism hotspot has emerged from recession to become one of Australia’s strongest economies and officially the nation’s best-performed property market for a couple of years (and counting).

Our motivation for investing significant resources on analysing markets is not about bragging rights or to win a glorified “tipping competition”.

Whereas most, if not all, other market analysts are forecasting markets for general commentary purposes, Propertyology is doing so because we are actively investing – every day – across different parts of Australia!

Propertyology’s skill in being able to correctly join the dots enabled dozens of people to invest in Hobart WELL BEFORE the boom and thereby benefit from 100 per cent of the growth cycle. We stopped investing in Hobart in 2016 and began focusing our attention on several exciting non-capital city markets.

Every day, our multi-award-winning buyers agents now get asked “where’s the next Hobart?”

To learn how Propertyology can help you find the right property, in the right location, at the right price, contact us now.