Calculating changes to your borrowing power

Promoted by Confidence Finance.

![]()

Finance experts are often asked questions about how different types of income/expenses change people's borrowing power.

When applying for a new loan, lenders generally will calculate your overall income and ensure it's higher than your overall 'assessed' expenses. The banks assess the new debt (loosely speaking) you take on at an interest rate of around 7-8% at P&I repayments.

How different types of income/expenses are treated generally depends on a number of factors, including:

(a) the type of income/expense it is;

(b) which lender you look at, they treat different types of income/expenses differently;

(c) how much you're borrowing;

(d) tax rate used;

(e) the banks assessment rate (the 'buffer') that they use to check whether you can service the new loan;

(f) other factors (do you have existing debt with them, interest rate changes, APRA changes, etc).

Given the array of factors, the most common answer given to questions about income/expense changes is that it depends. However, for ease of use, below are some quick ‘back of the envelope' guidelines.

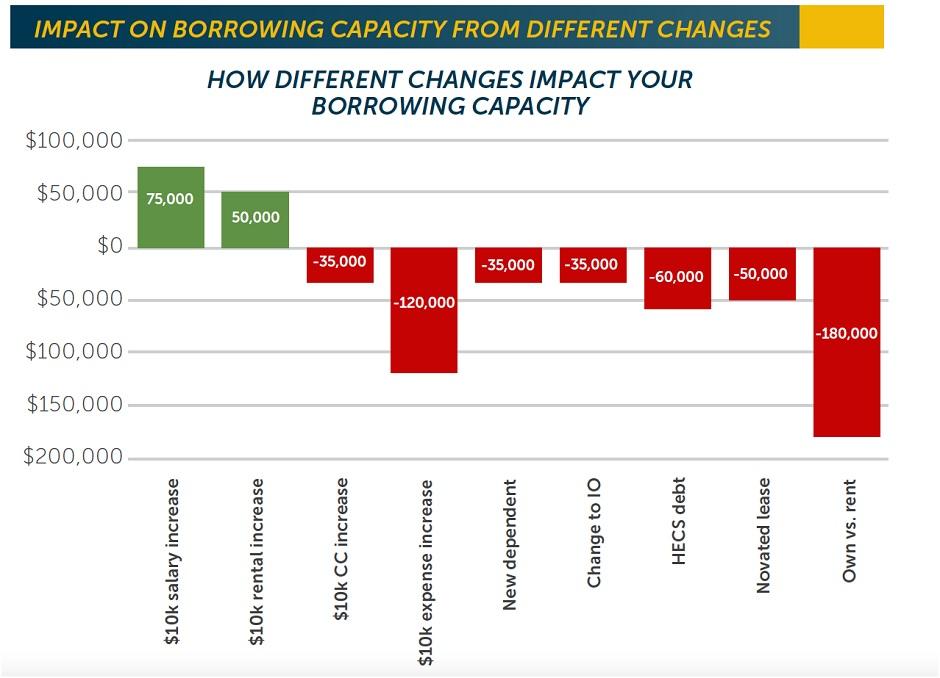

1. Salary/Business: Increase the average income earners salary by $10,000, will increase your borrowing power by ~$75,000.

The impact of this will fall for higher income earners, as they will pay a higher marginal tax rate. Given salary rises are potentially infinite, this is the most powerful way to increase your borrowing power long term.

2. Rental: For the average income earner, a $10,000 increase in rental income will increase your borrowing power by ~$50,000.

Can only include 80% of rental income generally. Therefore, it's a bit lower than salary increases. Note there is also an implied cap with many lenders, plenty won’t take yields above 6% into consideration (CBA, NAB).

Note, when there is investment debt against rental income earned, some lenders will allow those interest payments to be ‘added’ back to offset the taxation consequences of this income (negative gearing). When included, the rental income impact gets closer to salary rises.

3. Credit card limits: Increasing your limit by $10,000, will reduce your borrowing power by ~$35,000.

Credit card limits are generally assessed at 36% p.a. of the credit limit (regardless of whether you use it or not). This reduces your borrowing power by around $35-45k. Note a few lenders will exclude credit card limits if repaid in full every month.

4. Discretionary expenses (above bank minimums) - Increasing your expenses by $10,000 p.a. will decrease your borrowing power by ~$120,000.

Given this comes out of net income, it has more of an effect than gross salary increases. Given part of APRA changes increased minimum living expense figures banks had to use, this had a large impact on decreasing borrowing power.

5. Having another dependent reduces your borrowing by about ~$35,000.

Increasing the number of dependents adds at least $250 p/m to your monthly minimum expenses, depending on your current income level and the lender used.

Note, the impact of children usually has larger impacts with changes in income too.

6. Going Interest only on a loan for 5 years instead of Principle and Interest repayments on a $500,000 loan will reduce your borrowing power by ~$35,000.

One of the changes APRA forced recently was having banks apply higher effective assessment rates for interest only debt (via shortened loan terms).

Now, most lenders will assess a 5 year interest only term over a 25 year loan period instead of 30. For a $500k loan, this increases the assessed repayment by a little over $200 p/m, having about a $33,000 impact on your borrowing power.

7. Having ANY HELP debt on a median income will reduce your borrowing power by ~$60,000.

HELP repayments are based on a sliding percentage depending on your income. On an $80,000 income, 6% of your income is withheld to repay this loan. That means an additional expense of $400 p/m. This reduces your borrowing by around $60,000.

Therefore for some at the edge of servicing that have a small HELP debt, it may make sense to repay this loan. Repayments are based on income, not loan balance/size.

8. Obtaining a novated car lease for a $20,000 vehicle that includes all running expenses instead of a personal loan will reduce your servicing by ~$40,000-60,000.

Novated car leases usually include things like interest, fuel, car servicing, etc, into the monthly repayment amount, whereas personal loans usually have lower repayments because they only include the interest repayment. The other car costs can be included in the banks minimum living expenses for those that have personal loans. Therefore, Novated car leases do more damage as they potentially ‘double dip’ the living expenses.

Note the impact on borrowing power varies significantly depending on the specific arrangements of the lease. I’ve used an online calculator that breaks down the novated car lease costs for a $20,000 car – the additional running costs other than finance equate to around $400 p/m. This varies depending on finance terms, km’s driven (fuel cost impact), etc.

9. Deciding to buy a $500,000 property (100% financed) to live in vs rent @ $500 p/w will reduce your borrowing power by approximately ~$180,000.

The assessed expense for a $500,000 owner occupier mortgage debt is around $3.4k p/m (despite only paying $1.75k p/m in interest). If instead, that someone rented the same place at $500 per week ($2,166 p/m), lenders will take it exactly at $500 p/w in servicing assessment. No loading applied for rental expenses.

In this scenario, that’s a whopping ~$1,250 difference in your monthly expenses. Therefore, under some lender calculators, you’ll be able to borrow $180,000+ more for investments by making the choice to rent instead of buy in this scenario.

More analysis and a detailed explanation of how to manage your portfolio safely is available in our E-book: How to Grow a Multi-Million Dollar Portfolio.

At Confidence Finance, we believe that long term property investing is a game of finance and property finance is a science. Understanding how each part of lending works is our specialty. We use this insight to develop a unique understanding about how lending works in Australia. We then use this expertise to help our clients grow, finance and protect successful property portfolios.

About the author:

Redom Syed is the CEO & Founder of Confidence Finance. In 2017, he has been recognized as one of Australia’s youngest ever to reach the Top 100 brokers in Australia. Prior to becoming a finance specialist, Redom worked as a Senior Economist at Federal Treasury, where he became a published author on the design of the International Financial System.

More from this writer:

-

10 Smart Reasons to Refinance That Go Beyond the Interest Rate

-

Press Release Chamberlains Law Firm Expands with New Brisbane Office

-

New to Property? 4 Steps to Build a Strategic Portfolio

-

How Polished Concrete Can Increase the Value of Your Home

-

Ensure Your Next Investment Property Is Future-Proof – Key Due Diligence Steps Every Investor Must Take

-

Should You Build a New Home for an Investment Property?

-

How to increase value of your investment property?