Mortgage Tips For Self Employed- How To Increase Your Borrowing Power

If like most business owners, you try to minimize your tax to save on the hip pocket, sometimes you could be doing yourself some financial harm when it comes to buying a property.

SPONSORED BY Blogger: Neil Carstairs, Director & Senior Lending Specialist, Mortgage Corp

We’re going to show you an example of how planning strategically can set you up with great financial options in the future.

A tradie client, single, lived on his own. His accountant, like all ‘good’ accountants, had been trying to minimise the amount of tax he’s paying.

He wanted to buy a house and one of his friends recommended Mortgage Corp.

So he came to our office in Mt Waverley for a free mortgage strategy session.

After going through his goals, lifestyle, his current finances, etc, I advised him to speak to his accountant and pay as much tax as he could

He was confused, he had always been told to reduce tax in any legal way possible, but I explained how just paying a little more tax would benefit him in the long run and he would be able to buy a nice house in the suburb he liked.

Great business, descent savings, but banks won’t lend you money?

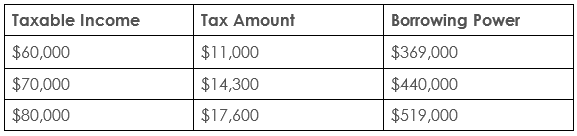

This tradie had a great business with good profit but thanks to his good accountant, he only had a tax income of below $60,000 for the 2 previous financial years. With the income he’s declaring, he was paying approx. $11,000 in tax for the year.

After some basic assessments, I told him based on his current taxable income, the maximum amount he could borrow was $360k. This means no bank will lend him enough money to buy the house he likes. And if he wanted to buy a property in the suburb he was interested in, he could only go for units and town houses.

He was shocked, “my business is making good profit and I’ve got $70,000 savings in my bank, I thought I was doing well…”

“A decent deposit is a good start, let’s have a look what you could do to get the house you wanted.” I took out my calculator and wrote down these figures:

By increasing around $6,000 in tax, you would have increased your borrowings by $159,000.

He could do a lot more with his new borrowing power.

$500,000 House + Investment Property

He followed my advice and came back to see me the next financial year with his tax return. Now he owns a house worth $500,000. He’s current renovating his home, as all good tradies should, and the renovations should help boost the value of the house when competed.

Upon completion of the home renovation, we’ll get his house re-valuated. We then plan to leverage the increased house value to buy an investment property.

This example shows that even on a very small scale how the benefits of getting as much advice as you can and proper planning can hugely impact on your borrowing power and your future lifestyle.

If you take only one thing away from this article it is that planning ahead and working with the right professionals can have a great impact on the success of your future investment.

Please note: every person’s situation is different, our goals, lifestyle and circumstances are different from our friends and family.

This is why, at Mortgage Corp, we always start with personal situation analysis on the free mortgage strategy consultation before going into loan products and interest rates etc., so we can make sure your mortgage is structured for long term investment success.

For specific tax advice, we suggest you to consult your accountant or we can recommend an accountant we’ve worked with and trust.

More from this writer:

-

5 Tips For Financing Your First Commercial Property Loan

-

COMMERCIAL LOAN CASE STUDY

-

What Is A Comparison Rate? How The Fine Print Is Costing You Thousands

-

CASE STUDY: Investment Property For An Extra $50/week

-

CASE STUDY: Investment Success With $0 Deposit $0 Mortgage Insurance

-

How Two Investors Increase Their Investment Opportunity By $230,000

-

How two business owners paid off $40K ATO debt through refinancing